~9%

Cost Decrease

$1,683/year in inventory savings.

Evaluated five forecasting models on 5 years of daily demand, optimized a continuous-review inventory policy via Monte Carlo simulation, and cut total cost by ~9% while sustaining ≥ 95% service.

~9%

Cost Decrease

$1,683/year in inventory savings.

≈95%

Service Level

Target met via simulation.

24

Fewer POs/Year

149 → 125 annually.

Simulation Results

10,000 Runs · Grid-Search

| Metric | Baseline R=92 · Q=42 | Optimized R=86 · Q=49 | Delta |

|---|---|---|---|

| Total Cost / Day | $50.94 | $46.33 | -$4.61/day |

| Service Level | 96.8% | 95.0% | -1.8pp (still ≥ 95%) |

| Holding Cost / Day | $30.48 | $29.21 | -$1.27 |

| Ordering Cost / Day | $20.46 | $17.12 | -$3.34 |

| POs / Year | 149 | 125 | -24 |

| Annualized Total | $18,593 / yr | $16,910 / yr | ↓ $1,683 / yr |

Exploration · Tableau

5 Years · Single SKU

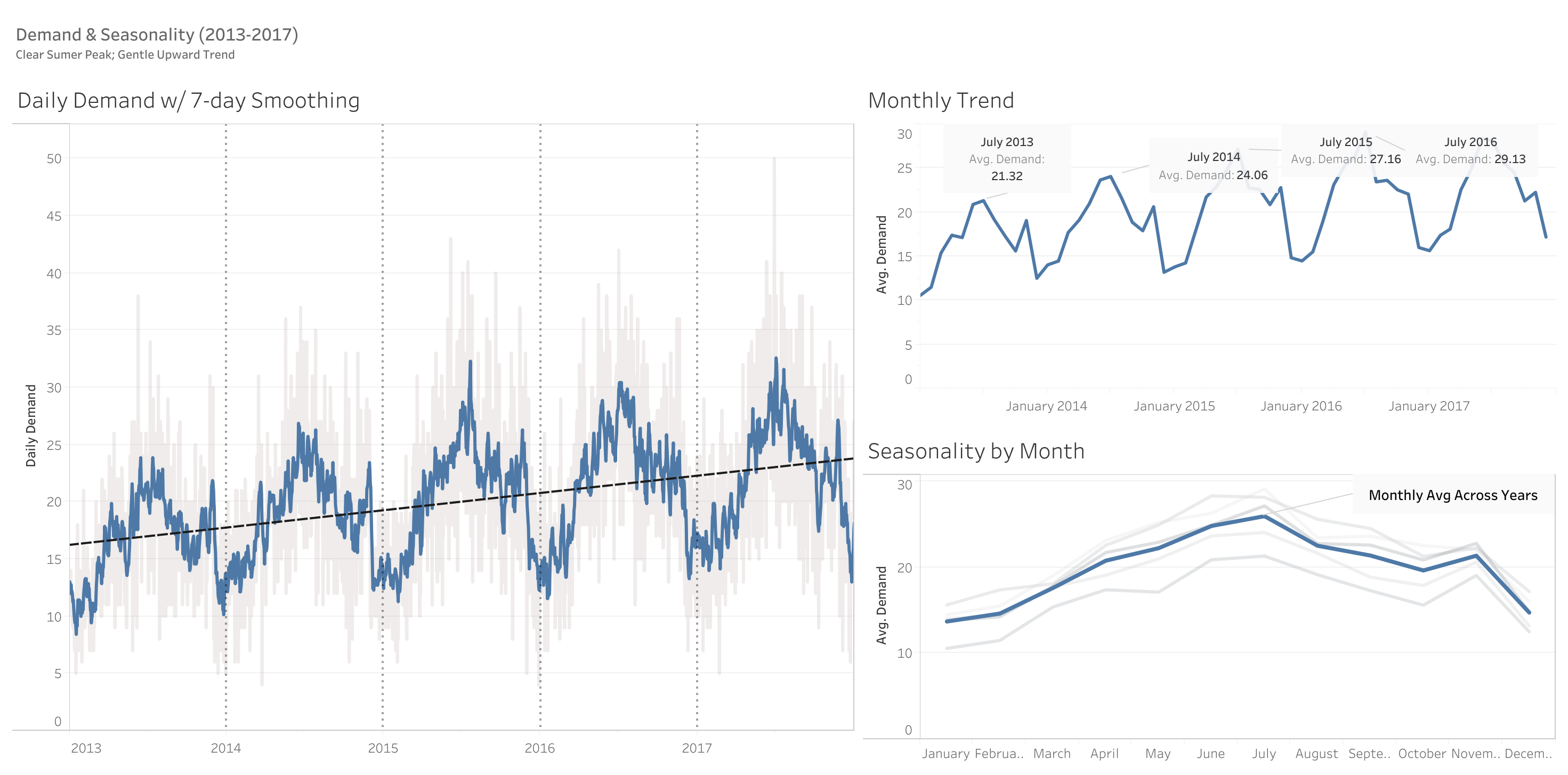

Exploratory analysis across 5 years of daily demand surfaced a clear upward trend, recurring monthly seasonality, and high day-to-day variability.

Methodology